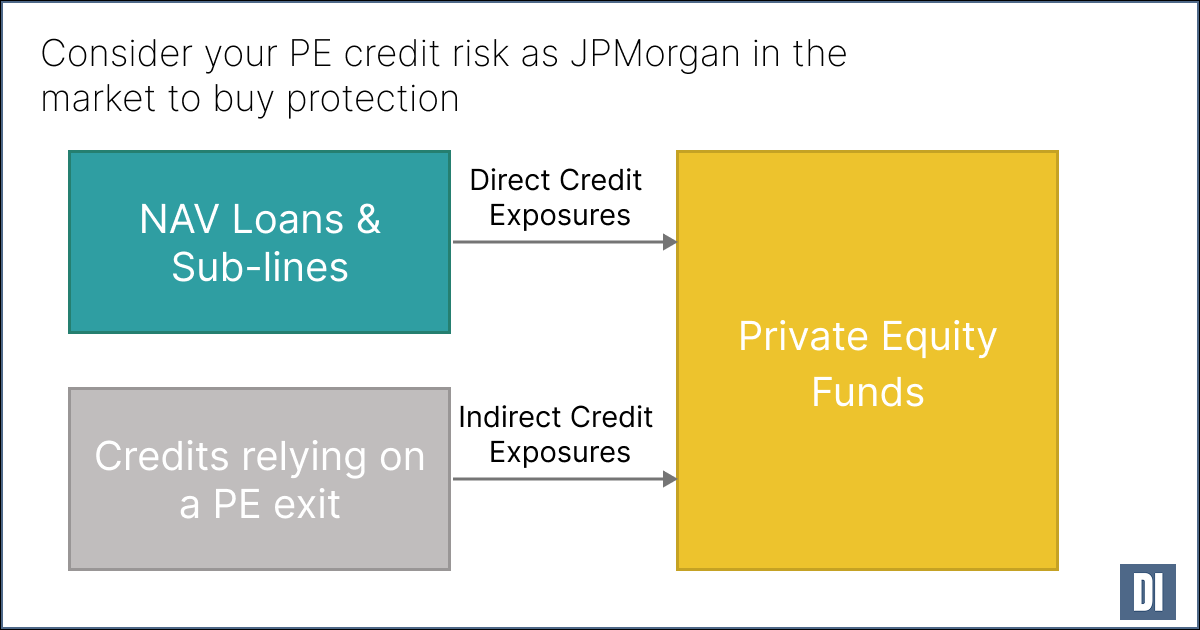

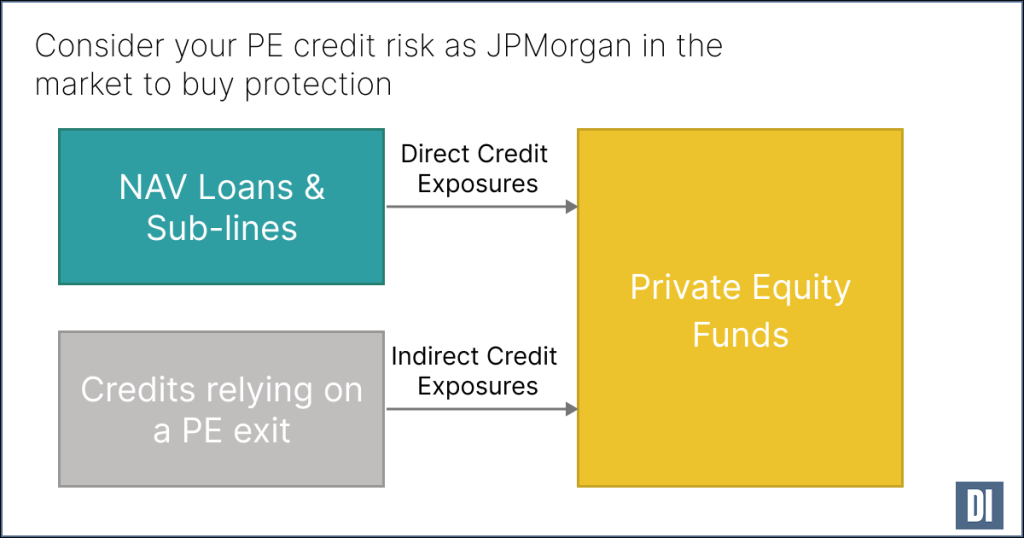

JPMorgan is reportedly in the market to buy credit protection on a $4 billion pool of NAV loans it has made to private equity funds.

NAV (Net Asset Value) loans are made to private equity funds and backed by the value of the stakes that the fund holds in companies (its assets).

Write-down worries

There are worries about write-downs in some parts of the private equity sector – including around portfolio companies whose business models could be disrupted by AI (currently focused on some types of software companies), and around portfolio companies that were invested in during an ultra-low interest rate environment and could be impacted by a possible new normal of persistently high (or very high) interest rates.

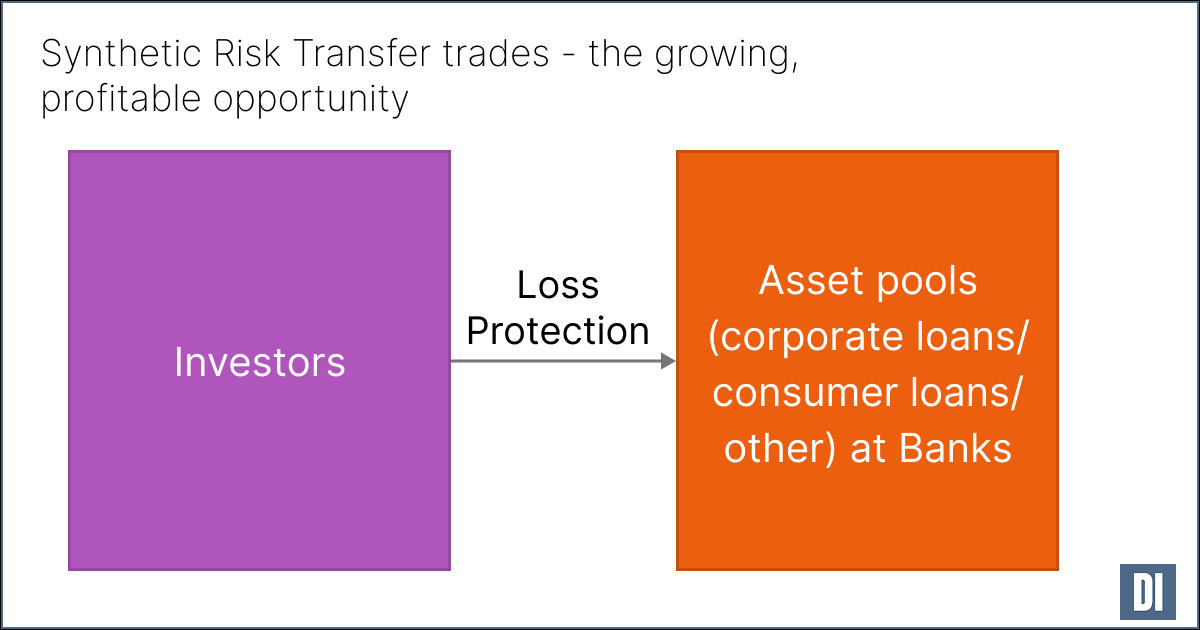

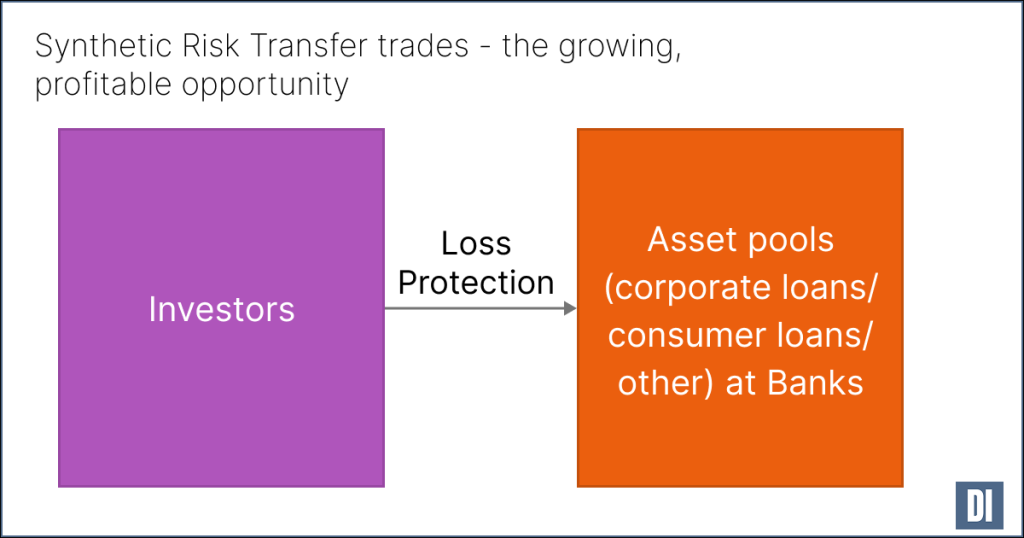

JPMorgan’s SRT transaction

JPMorgan’s transaction is reported to be looking to buy 12.5% first-loss protection on a portfolio of $4 billion of NAV loans at a low-teens yield.

This may be because JPMorgan is managing risk and it sees potentially higher risk in its NAV loans. It could also be for other reasons – for example, it might be a normal exercise to reduce regulatory capital requirements, or the bank may be doing this exercise to free up capacity for new NAV lending (a normal synthetic risk transfer/SRT trade). They could be freeing capacity to support new upcoming demand from their private equity client relationships, or they could be anticipating a period of stress in private equity – and creating balance sheet space to make future highly attractive new loans and to build long-term market share among private equity firms.

Looking at your PE-linked assets

For other firms, there has clearly been a change in the private equity industry – and there are likely to be further changes coming. It might therefore be a time to evaluate your exposures and future plans – both in protecting against risks and being ready to capitalise on opportunities. You may want to:

- Identify direct and indirect PE credit exposure that you hold – including NAV or sub-line loans, but also credits that rely on future PE support/exits as part of their credit stories.

- Form a view on what is likely to happen in the private equity industry over the next five years.

- Identify possible risks and opportunities from these changes.

- Identify which of these risks and opportunities you might want to take action in relation to now.