Synthetic Risk Transfer (SRT) trades are a fast growing source of revenue for issuer banks, private credit investors, insurance companies, asset managers, hedge funds, investment banks and law firms.

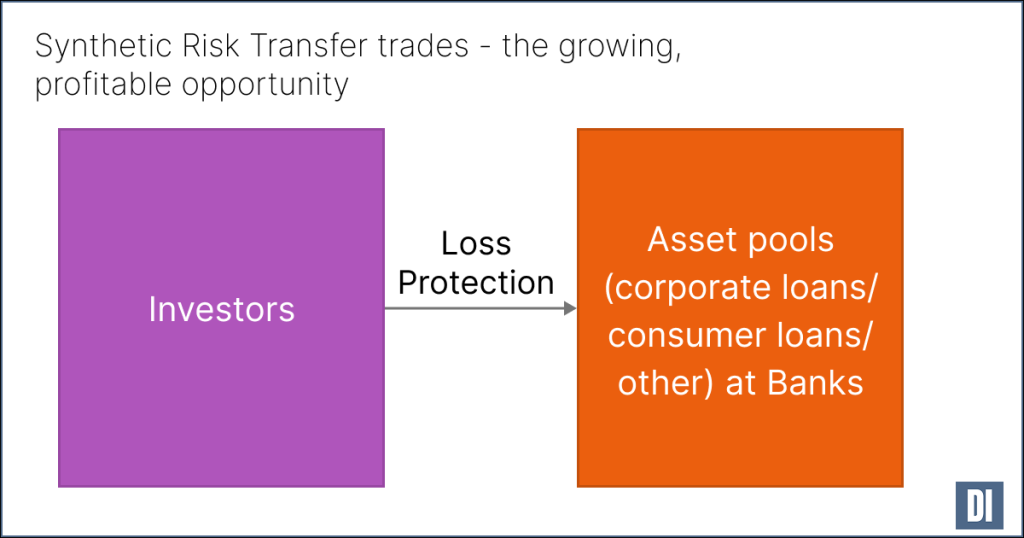

These trades are like buying insurance – where banks pay investors to protect them from losses on a specific pool of assets that they hold (this pool of assets are often corporate loans, SME loans, consumer loans or auto loans).

The market is large (over $1 trillion of assets protected since 2016) and growing rapidly.

It is growing both because the asset class is becoming more established (more investors, more precedents, more laws/regulations created to support SRTs), but also because Basel III 3.1/Endgame rules are creating new opportunities for banks to reduce capital costs by using SRT trades.

The deals are typically structured as an unfunded bilateral credit default swap (CDS) or as a funded credit-linked note (CLN).

One of the “trades” that investors look for here is – find assets which are treated “wrongly” by bank capital regulations – where the regulations require banks to hold a lot of capital against those assets (because they assume they may incur high losses), but investors think that the riskiness of those assets is actually much lower.

The opportunities

Issuer banks – SRT trades allow banks to reduce the regulatory capital they need to hold against assets they hold – which in many cases allows them to more than double their return on capital for those assets. These trades can also be used for commercial reasons – like allowing a bank to continue to lend to a particular company or sector, even if they would otherwise be approaching the maximum concentration of risk they want to that company or sector.

Investors – Investors can find assets that they consider to be high expected return. Many deals yield high-single-digit to high-teen returns. It allows investors to deploy relatively large amounts of capital at scale – both because individual deals can be large but also because investors can create a process to originate multiple transactions in one category (as an example SRTs on German auto loan portfolios). These deals were historically done by investment banks and hedge funds, and then increasingly by private credit funds, and now insurance companies, pension funds and asset managers are becoming buyers.

Investment banks – The SRT market is still far from saturation. Demand is growing among banks – among large and medium sized European and US banks (the category of issuers we have mostly seen so far), but also smaller EU, UK and US banks, and emerging markets issuers. It also supports the investment bank’s distribution platform – as it provides investors with interesting, potentially high value product that they can’t easily get from many sources. The complexity of these transactions – including working out cross border regulations, capital rules and modelling large asset pools – allows arrangers to charge high fees.

Law firms – SRT deals need high-value cross-domain work that needs expertise in banking, regulatory, capital markets and increasingly insurance law. The set of law firms who do this work is still relatively small – allowing law firms to compete in a high value, low competition market.

In general: as these trades are relatively complex from a structuring perspective, because they have special risks, and because the asset class is growing rapidly – it offers potential opportunities that have lower competition/higher profit than in other areas of the debt capital markets for firms that can manage this complexity.