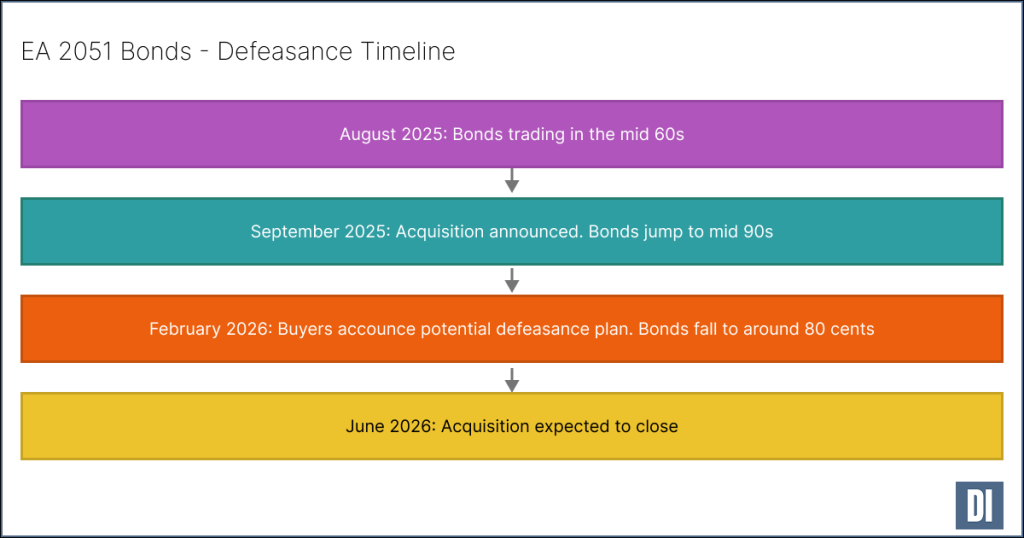

Electronic Arts (EA) acquisition by the consortium of Silver Lake (private equity), PIF (the Saudi sovereign wealth fund) and Affinity Partners (private equity) was announced last year and is expected to close by the end of June this year.

When the deal was announced, EA’s 2051 maturity bond prices went up from trading in the mid-60s to trading in the mid-90s – as investors thought that the “change of control repurchase event” provision in the bonds would result in the bonds being bought back soon at slightly above par (at 101 cents).

The bonds were trading in the low 60s largely because they were issued in 2021 – and 30-year treasury yields have increased by over 1.5% since then (so need to discount the bond by a 1.5% higher rate over the next 25 years).

So an immediate redemption at par (actually 101 cents as in this bond’s documents) would have been a big win for bondholders. Instead, EA used a defeasance option available to them under the bond – where they place treasuries as collateral against the bonds.

Primer on defeasance

Defeasance is an option that may be included in a bond’s indenture document. It allows an issuer to legally satisfy its obligations with respect to a bond in some way. The issuer is legally discharged from the debt – meaning it can be removed from their balance sheet even though the bonds are still outstanding. This is usually by depositing enough treasuries with the bond trustee to be able to pay back the full principal and interest due under the bonds to their maturity. The exact mechanism differs by bond and is laid out in the bond’s indenture document.

This resulted in EA’s 2051 bond’s prices falling from around 95 cents to below 80 cents. Because investors still need to discount the cashflows by the higher current interest rate than when the bonds were first issued. On the plus side, they have no credit risk against EA (as the bonds are now collateralized by treasuries) – so that gives us a higher price than the low 60s level the bonds were trading at before.

Expected outcomes for EA’s 2051 bondholders

| Scenario | Possible expected value | Logic |

|---|---|---|

| Change of Control Put trigged | 101 | The bonds would have been bought back within a few months at 101 cents |

| Defeasance | Mid 70s | The bondholders still hold the bonds. They still suffer from a higher long term interest rate environment now than when the bonds were issued in 2021. But they no longer have EA’s credit risk (they are backed by US treasury bonds). |

| Pre-acquisition announcement | Mid 60s | Interest rate discount + higher EA credit risk |

This is a good case study for private equity funds and for bond investors. For private equity funds, it can in some cases allow them to pay more for a leveraged buyout (which is important in the currently competitive market for private equity deals). For investors it is a good reminder to work through the bond’s indenture documents in detail and play out what could happen. There was potentially an opportunity for investors to make a very quick profit here by spotting this opportunity and shorting the bonds when they traded in the 90s.

The bond’s indenture document if you want to see the provisions: Indenture – SEC Filing. The Change of Control Repurchase Event is explained on page 13, and the Defeasance mechanism is explained on page 21.