Blue Owl Capital Inc is one of the world’s largest private credit fund managers.

They have been in the news because they have stopped investors in their retail-focused private credit fund from being able to redeem 5% of their investment each quarter. This has led to worries about private credit assets being overvalued across the market.

The key issues

1) Can private credit valuations be relied upon? There is no good market price for many private credit investments, and investors often need to rely on the judgement and unbiased views of the people making the valuations.

2) Worries of hidden “bad loans” across the private credit industry. There are questions about whether there are a lot of “bad loans” hidden across the private credit industry.

3) Risk of a private credit crisis and a broader credit crisis. Because of how big the global private credit markets have become ($3 trillion+), there is a chance that a private credit crash could have large knock-on effects in the financial system, and that it could reduce credit availability in the real economy – resulting in lower GDP, employment and asset prices.

“The story” – what has happened with Blue Owl’s OBDC II

Blue Owl Capital Inc is one of the world’s largest private credit fund managers. They are listed on the NYSE.

The short version of the story – Blue Owl has a retail fund called OBDC II – which allowed investors to redeem 5% of their investments each quarter. Blue Owl made changes last week which stopped investors from being able to do this – and this has caused broader worries about the private credit markets.

The longer version –

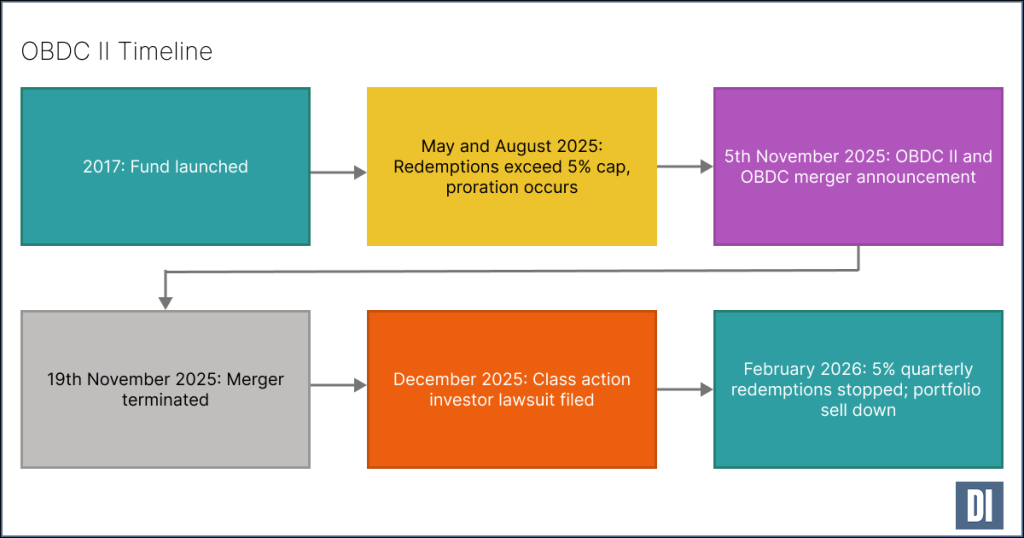

Blue Owl has various private credit funds – including OBDC II which is targeted at retail investors. OBDC II is not listed and directly lends to US middle-market companies. It held investments in 190 companies with a stated NAV of $1.7bn (as of September 2025).

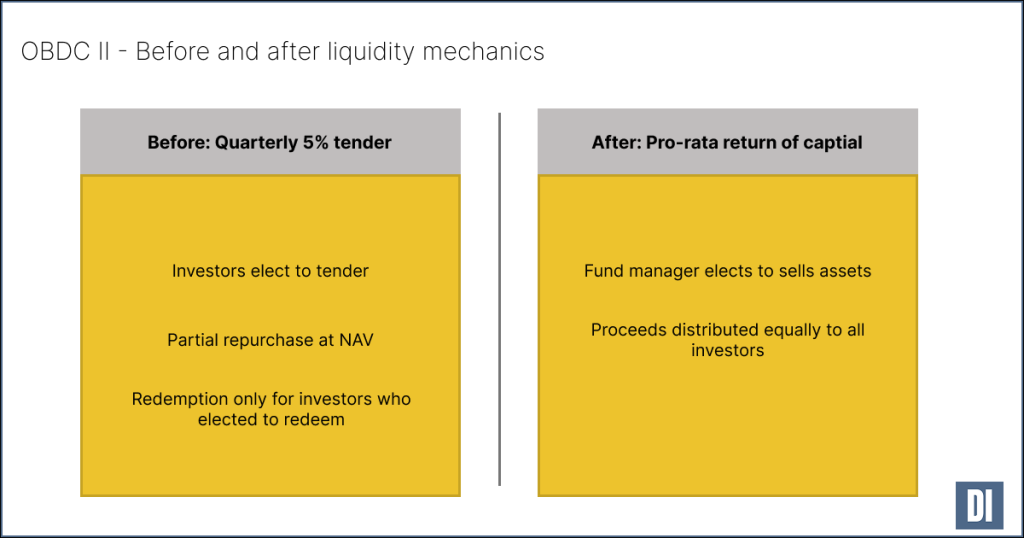

Investors in OBDC II were able to redeem up to 5% of their holdings every quarter. The problem that Blue Owl faced is that the full 5% was starting to be redeemed each quarter – and it seems that Blue Owl was not able to do this without causing losses for the rest of the fund.

This might be because of liquidity problems (it could not sell 5% of the loans at their marked value each quarter – but could sell them at their marked value with more time), it might be because of overstated valuations (the valuations on the loans should actually be lower than they were marked – because these loans are opaque it is easy to make mistakes on their valuations), or because of something else.

Blue Owl tried to solve this by trying to merge OBDC II with a listed fund late last year (as then there would have been no more redemptions – investors would just sell their shares on the market when they wanted to sell) – but this would have resulted in a (paper) loss for OBDC II investors as the listed fund was trading at a 20% discount to its NAV – so OBDC II investors pushed against the merger and so that plan was called off.

An investor lawsuit was filed in January 2026 claiming that Blue Owl misled investors about redemption pressures in its business development companies and about the likelihood of curbing redemptions.

Then last Wednesday (18th February 2026) Blue Owl released a statement that meant that investors would no longer be able to redeem 5% of their investment each quarter. Instead, Blue Owl would start selling down some of the portfolio and return proceeds from those sales to all investors in OBDC II.

OBDC II sold almost a third of its portfolio as the first such sell down. It sold $600m of its portfolio at close to par (99.7%). It will use the proceeds to repay a credit facility from Goldman Sachs and return funds to shareholders (around $538m – worth around 30% of the fund’s NAV).

Some hedge funds including Saba Capital and Cox Capital last w eek announced that they will offer to buy shares in OBDC II from investors at 20% to 35% below NAV.

The biggest question – is this an indicator of bad loans across private credit

The biggest question is whether this event is an indicator that a large proportion of loans across the private credit industry are overvalued. The market is opaque (there are no traded prices as there are with liquid bonds) and information around a lot of private credit loans across the market is secret.

There are worries that this change by Blue Owl is because they could not sell a big enough representative slice of the OBDC II portfolio each quarter to cover redemptions at the prices that the loans are currently marked. There is also a worry that Blue Owl was forced to make this change because OBDC II’s creditors (for example Goldman Sachs whose credit facility was repaid) required it.

Even with the block sale at close to par (99.7%), the worry is that this does not reflect the actual value of the entire loan book of OBDC II. There are worries that it could be a friendly deal – at prices higher than they should be, and/or that the loans sold were effectively “cherry picked” – where the best/easiest to sell loans were sold, and a large proportion of the remaining portfolio contains loans that are marked above where they can be sold (a “toxic tail”).

What we might see happen with OBDC II

We might see OBDC II continue to run – with more block sales over time. The timing of these sales seems uncertain – they could happen quickly or it seems they could take very many years. It might turn out that the loans can be sold around (or above) current NAV – or it might turn out that some of OBDC II’s holdings end up being marked down over time.

Manager backstop – Another interesting thing that could happen here is that Blue Owl could step in and support OBDC II. Blue Owl is a large, listed asset manager ($300bn+ AUM and $17bn market cap). OBDC II is small in comparison – at a little over $1bn AUM after the announced block sale is completed. This OBDC II issue is, however, causing a lot of noise for Blue Owl, affecting its share price (down 25% in the last month), and could affect its AUM if other investors avoid the noise around this and pull assets under management from Blue Owl. Blue Owl might be able to find relatively inexpensive ways to support OBDC II. We saw Blackstone support its retail focused real estate fund BREIT when it had redemption issues in 2022/2023 by providing a $1bn backstop and a guaranteed annualized net return of 11.25% to secure a $4bn investment from the University of California into the fund. This might be what funds like Saba and Cox which are offering to buy shares in OBDC II at a discount are betting on.

Effects on the broader private credit market

Risk of private credit market contagion – there is a chance that this event changes perceptions towards private credit, and then that relatively quickly creates a negative cycle of investors selling private credit, prices falling (in an illiquid market), and then more sales. This is by no means a given (or even a high probability case) – but given the size of the impact if it did happen, should be considered by market participants.

This is an isolated event and the private credit market continues to develop – there is a chance that this is quickly seen as an isolated event (related to a suboptimal structure for giving private credit access to retail investors), and the private credit markets continue to develop. This event could even play a part in developing the secondary markets for private credit.