Apollo Global Management’s co-president, John Zito, warned at a UBS event that recoveries on mid-market software loans for some companies taken private between 2018 and 2022 could be “somewhere between 20 and 40 cents”.

The 2018 to 2022 period saw high valuations for software companies, and close to zero interest rates. AI fundamentally risks the business models of some of these software companies, and interest rates have risen a lot since then.

This may in part be an attempt to position Apollo as a safe manager in a difficult period for the private credit industry – as Apollo has said they have a small exposure to software companies.

But his insights might also be accurate. This fits with the credit markets’ usual “bubble creating” mistake of over-relying on stable historical data to predict future cashflows (over fundamental, future-focused market analysis and modelling).

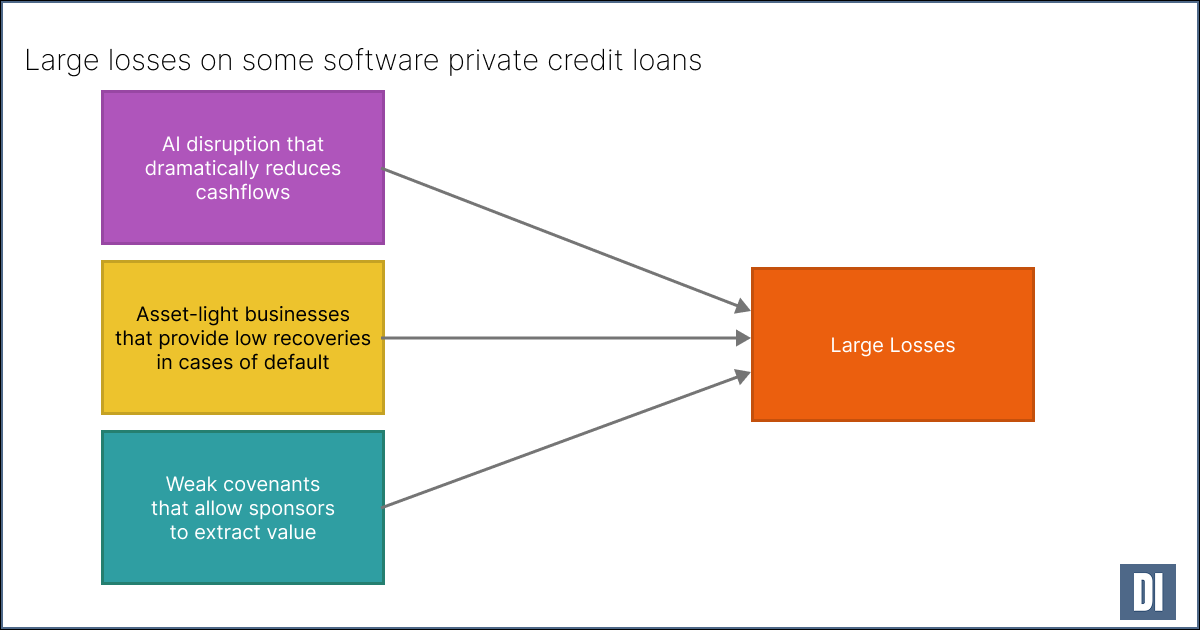

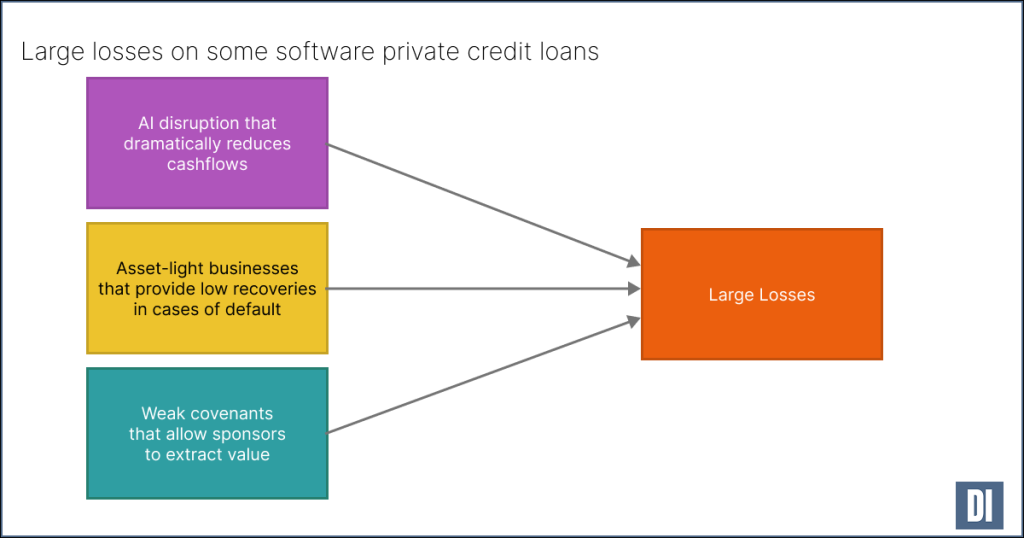

For some software companies that are disrupted by AI, stable historical cashflows might quickly fall – potentially making covering interest payments and refinancing difficult – which could result in a large number of defaults. As software companies are usually asset-light, recoveries might be particularly low relative to other sectors.

Why this might overstate the problem in software private credit

There is likely to be a range of outcomes for loans to software companies.

Future cashflows: Software companies are not built equal – some software companies will do well in an AI world. Some will fare terribly. This will depend on things like their client base (retail or enterprise), how much proprietary data (including user data) they have and use, and how much of the service they are providing is truly software and how much of it is non-software (possibly disguised as software).

Debt profiles: There will be a range of debt profiles – loan maturity profiles and loan terms. These will both affect how likely each company is to default, and what the recovery is for each investor. Many of the 2018 to 2022 software company LBOs were financed with unitranche structures – with agreements between lenders behind the scenes, which tranches repayments and recoveries among lenders.

We have seen this type of deal already see some markdowns. For example, private credit lenders including Blackstone have been marking down their private credit loan exposure to marketing technology company Medallia, which was acquired by private equity firm Thoma Bravo in 2021. Some lenders have already marked this loan down to 77 cents.

The big hidden risk – systemic risk: Private credit firms have been taking leverage from banks (“back-leverage”) on their private credit portfolios. An unknown risk is whether there is the risk of a systemic unwind here – where positions are marked down, triggers are breached in back-leverage, funds are forced to sell private credit positions, secondary-market private credit prices fall with increased supply/forced sellers, and that then further reduces valuations.

Potential opportunities

This environment could throw up opportunities for banks and investors.

Sorting credit quality: There are likely to be many private credit loans that end up with large losses, but there are also likely to be many private credit loans which turn out to be very high credit quality and continue to be valued around par. Being able to work through the private credit universe might allow investors to find loans (or funds) which are strong credit quality and at some point end up dramatically underpriced. There might also be opportunities to short assets which investors assess could fall significantly.

Leveraged finance: Some companies (and their sponsors) might start to find they suffer from pressure as financing maturities come up, or as they come up towards breaching covenants. There might be a considerable amount of M&A at that point – which will need debt funding, in an environment in which debt funding supply is limited. This might create opportunities to build portfolios of strong, well-structured, high-margin loans for leveraged finance providers who can effectively assess quality. It could also allow new or small leveraged finance providers to build a franchise that could then create value well beyond this credit cycle.