Defence DCM – across bonds, private credit, securitisation and leveraged finance – is likely to grow very rapidly.

Why: geopolitical changes mean trillions more of defence spending and changes in end investor perceptions

Geopolitical changes have changed how the public and end investors perceive defence investments. They have moved from being seeing as a destructive industry to avoid, to one that is necessary for peace and security.

There are two important changes for debt capital markets participants that follow from this: 1) governments are spending MUCH more on defence – estimated to increase from $2.6 trillion/year now to $7 trillion/year by 2035; 2) end investor perception has changed – with many more investors now willing to invest in defence related assets. As an indicator of the second – defence sector bonds are now being included in some ESG frameworks.

So what: CapEx, working capital and M&A

The magnitude of this potential additional spending on the debt capital markets is difficult to overstate – with defence-related credit potentially becoming a major part of the bond, private credit, leveraged finance and securitisation markets.

Credit markets will: i) fund CapEx, ii) fund working capital, iii) fund M&A.

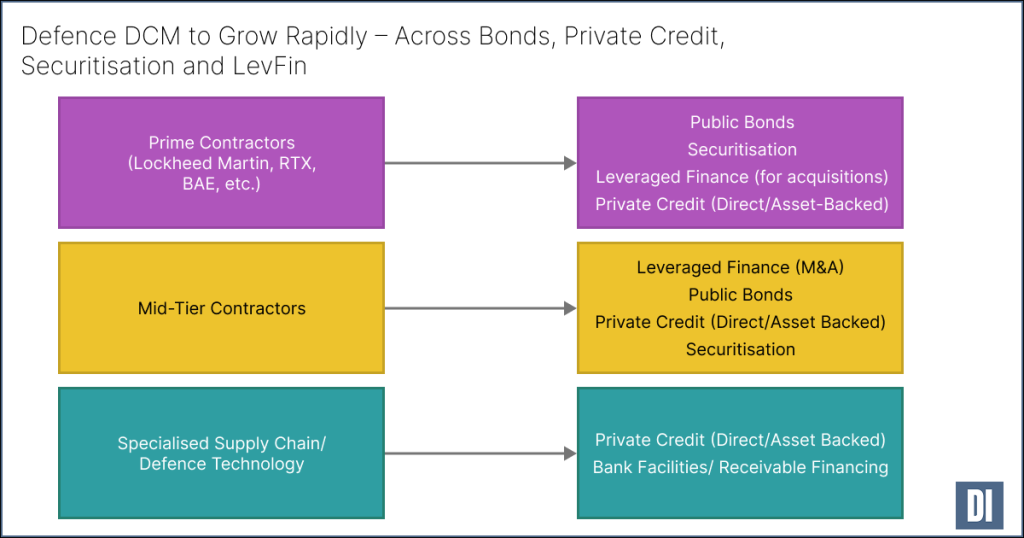

By market: levfin, working capital, private credit, securitisation

Leveraged finance

Potential for a LOT of M&A. The market is highly fragmented below the largest players (the “Tier 1 Prime Contractors” like Lockheed Martin, RTX, Northrop Grumman, etc.).

Working capital

There could be hundreds of billions of working capital needed to finance production – with production taking years for some products.

Private credit

Many deals will be well served by private credit funds – with fast, flexible, confidential deals. This may allow managers to offer LPs a private credit premium over public credit. Managers have started launching specialist defence-linked private credit funds. These recent funds include Sienna Hephaistos Private Investments, Grays Peak Private Credit II, Leonid Private Credit Fund I.

Securitisation

Potential for hundreds of billions of dollars of public and private asset backed financing for capex and of receivables. Receivables will often by government-linked.

For participants: investors, private credit, issuers, investment banks, law firms, governments

Bond investors

Consider allocation to defence sector credits. Possible that current [10 to 30] bps defence bond premium will fall. Possible that end investor demand will grow rapidly. Potential for diversification – including if there is a recession.

Private credit

Consider investment in defence sector credits. Explore demand for specialist defence sector funds among LPs.

Issuers

Explore new funding options. This could provide an edge that allows primes and subcontractors to be able to beat competitors on costs and win new mandates. Being an early mover in the capital markets could also provide a significant competitive advantage by becoming known by investors, building a track record, and being able to raise more credit at lower costs than competitors. This may also affect how M&A plays out – which companies end up being the acquirers.

Investment banks

Consider positioning for origination, structuring and distribution of defence credit. Look at new defence funding programs including the EUR 800 billion EU ReArm Europe Plan, $1.5 trillion “Security and Resilience Initiative”, the EUR 150 billion Security Action for Europe (SAFE) program.

Law firms

Explore growing your defence sector debt capital markets capabilities – including various new Defence Bond frameworks, new ESG/ESSG (with “Security” added) frameworks, special risks for investors and arrangers in defence sector deals, due diligence for these risks.

Governments

Consider developing Defence Bond labels. Consider legal and economic protections for investors in the defence sector. Consider programmes to support investments in your defence industry.