What does SRT stand for?

Significant Risk Transfer or Synthetic Risk Transfer. Significant Risk Transfer is the original term and is still more commonly used.

SRT deals used to mainly happen in Europe, but their use has grown quickly in the US over the last couple of years because of US regulatory approval for them in September 2023. In the US, the term Synthetic Risk Transfer is commonly used. The terms Credit Risk Transfer (CRT) trades and Capital Relief trades are also sometimes used.

How large is this market?

The total assets protected through SRTs since 2016 is over $1 trillion. Just last year, this number was over $600bn. The amount of issuance is growing quickly, as the US has only recently entered the market.

With recent global political changes, financial markets competition between jurisdictions looks like it will increase. This is likely to result in regulatory changes around the world that accelerate the adoption of SRT trades.

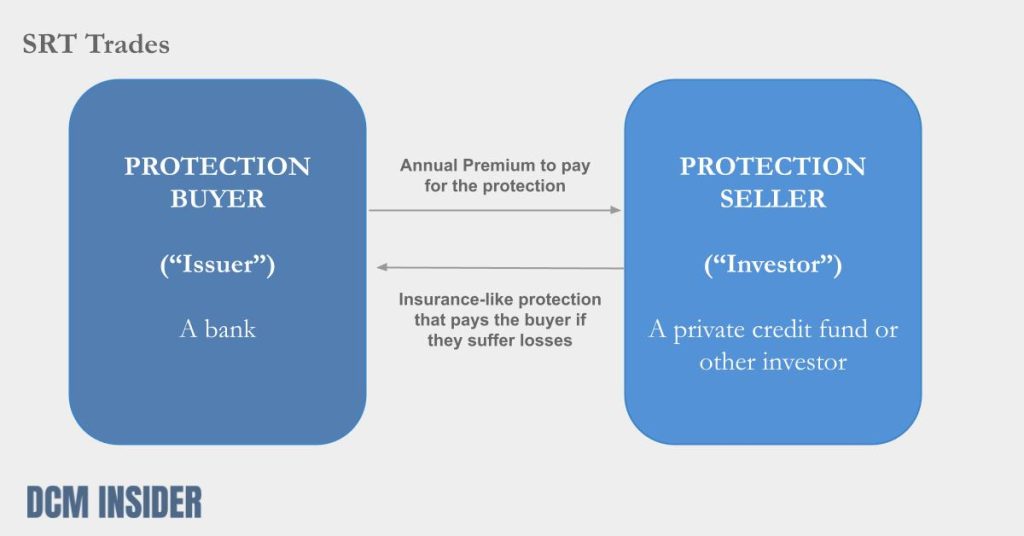

What are SRT Trades?

In short: SRT trades are a way for banks to buy insurance-like protection on some of their assets.

Who are the parties involved?

1) A protection buyer: this is usually a bank. This party is also called the issuer.

2) A protection seller: this is usually a private credit fund, investment bank, insurance company, pension fund, supranational, or hedge fund. This party is also called the investor.

Why do banks (protection buyers) do these trades?

The main reason is that it can be profitable – as the amount of regulatory capital that this type of deal frees up can be more expensive to hold than the amount they have to pay for the deal.

For example, buying protection on a set of assets might cost a bank $3 million per year in premiums that they need to pay to the protection seller; but the bank might save $5 million per year because of the amount of regulatory capital it frees up for the bank.

Are there other reasons banks might do these trades?

This is less common – but in some cases banks might have too much of one type of risk and could use an SRT trade to reduce their concentration of that type of risk.

For example, a specialist bank in Greece might have a lot of exposure to shipping loans relative to its total asset base – and so may enter into an SRT trade wherein they buy protection on some of their shipping loans – and so reduce their total exposure to shipping loans.

Why do protection sellers (investors) do SRT trades?

Investors get paid to take the risk.

Because these trades are relatively complicated to understand and put together, they face less competition than many other types of investment. This creates an opportunity for investors who have the right expertise in their teams. It can allow them to make investments in SRT trades that pay a higher return than other investments with the same level of risk.

What risks do banks protect against in SRT trades?

Usually against losses in portfolios of loans that the bank has made to customers – like residential mortgage loans, consumer loans, auto loans, or corporate loans.

How do investors evaluate the risk they are taking with SRT trades?

Investors usually put together a model – that tries to estimate the risk of having to make a payment because there have been losses on the assets that the SRT trade protects. They will usually use broad market data (like economic projections) and specific data (like historical default rates and losses that the issuer has experienced on this type of asset).

What unlocked SRT Trades in the US in 2023?

Clarification from the US Federal Reserve in their September 2023 FAQs made it clear that these deals work in reducing regulatory capital requirements for banks the US.

How are SRT deals structured?

SRT trades are mostly structured as Credit Default Swap (CDS) contracts or Credit Linked Notes (CLNs). In either case the protection buyer gets paid out by the protection seller if there is a loss event on the protected assets.

The difference is that CDS contracts are usually unfunded and CLNs are funded upfront. Because of this, when a loss event happens, with a CDS the protection buyer needs to ask the protection seller to transfer money to cover the losses; but with a CLN, they just deduct the loss from the money they already hold on behalf of the protection seller.

CDS can be cheaper, but expose the protection buyer to the credit risk of the protection seller going bankrupt – meaning that CDS can only usually be issued by highly-rated protection sellers. There are also regulatory differences in different jurisdictions that affect exactly how these deals are structured in different markets.

These deals are usually structured in a way such that there is a cap on the amount of losses that the protection seller will cover. For example, on a $100 million portfolio, the protection might only be for the first $10 million of losses. Similarly, there might be the equivalent of an excess on an insurance policy – where the first losses on the portfolio might have to be borne by the issuer. In our $100m portfolio example, this might be that the first $1 million of losses are not covered. This is referred to as “tranching”. These caps and excess-like provisions are structured on a trade-by-trade basis based on what each party is trying to achieve, regulatory rules in the jurisdiction, and other factors.