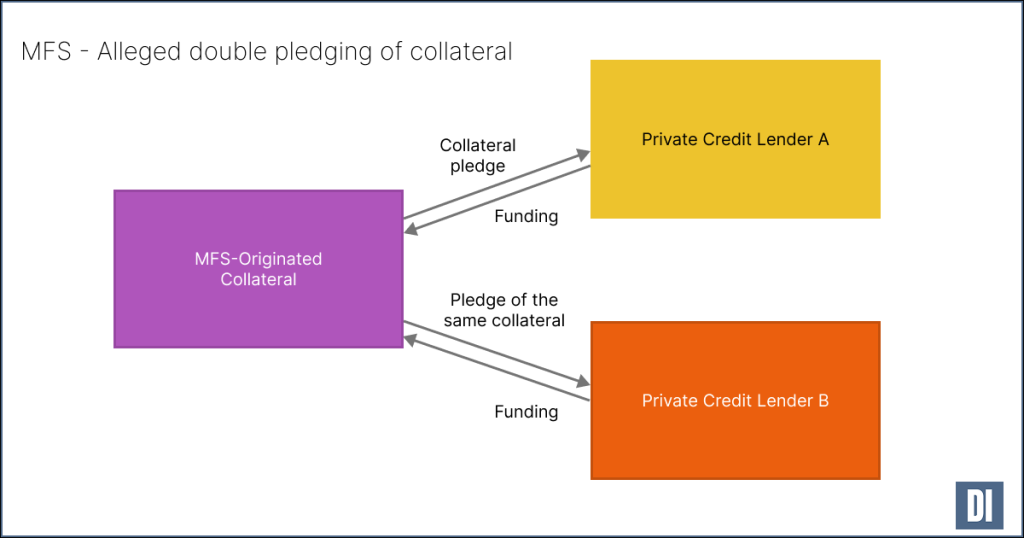

Market Financial Solutions (MFS) is a specialist UK mortgage lender, that borrowed in the private credit markets from many leading private credit investors. Allegations include fraud – providing false information to lenders and pledging the same collateral to multiple lenders. This individual case is not systemically important (as the borrower is relatively small with a total loan book of £2.4bn at the end of 2024) – but what is systemically important is how it changes our view on whether there is hidden systemic risk from fraud and bad underwriting across the private credit market.

MFS was put into administration in late February. This follows the collapse of other private credit borrowers on counts of alleged fraud including US-based auto parts supplier First Brands Group and US-based subprime auto lender Tricolor Auto Group. Double-pledging of collateral is also an issue in the First Brands and Tricolor cases.

This set of events makes it more likely that there are hidden issues in parts of the private credit markets – around poor underwriting and servicing (including not spotting fraud).

Investors included Barclays, Apollo’s Atlas SP Partners, Jefferies, and Santander. The lending seems to largely be in the form of warehouse facilities.

This is likely to dampen parts of the private credit market – while investors assess potential losses, and private credit lenders strengthen their underwriting and servicing processes.

What to watch for next

Fraud at other mid-market originators: Watch for further private credit defaults from fraud. Private credit lenders are increasingly conducting deeper investigations into their investments in this type of company – which is likely to uncover fraud in some other cases. So we should expect to see some new cases come to surface in the coming months. The number of new cases that arise will help provide some feel as to how big an issue this is for the private credit markets.

Mid-market private credit drying up and being the CAUSE of financial distress for mid-market originators: Private credit lenders are increasingly under pressure over this type of investment. This is likely to mean that they will pull back from some existing and some new investments to this type of lender. As many lenders will not have a similar source of borrowing (with warehouse facilities being relatively unique – being able to provide high levels of leverage at low rates), expect to see some lenders shrink or collapse simply because they can no longer access the funds they need.

Changes in deal structures and underwriting requirements: Borrowers had a lot of negotiating power over the last few years – with large amounts of private credit capital that needed to be deployed and relatively few good investments available. This allowed originators to set many of the terms for the deals. This has changed with these defaults. Expect increased covenants, more transparency, closer monitoring, more auditing, and higher requirements on counterparties (who the trustees and administrators for the deal are, who the auditors are, etc.)

Worst case – wider contagion – from lower credit affecting asset prices: If mid-market originators find it more difficult to get credit, we might find this translate into the markets they service – for example for the types of bridging loans for residential property that MFS provided. This could cause asset prices in those markets to fall. This could in turn reduce the credit quality of private credit investments in this space – creating a negative asset-price/credit availability spiral.

Opportunities

These situations are fast-moving and complex. Being able to differentiate between creditworthy and risky investments in the mid-market originator space could provide investors with trade opportunities.

Investors who are able to better underwrite and service private credit to these mid-market originators might find an opportunity to find high risk-return investments. This could particularly be the case for investors who can get very hands on – deeply tapping into and monitoring the real-time data of lenders and closely auditing their assets.

There may similarly be excellent opportunities to buy secondary positions for institutional investors who are better able to assess the risk of these deals. There might be some particularly attractive opportunities for subordinated tranches.

Legal and regulatory effects

Now that there are multiple cases of alleged fraud related to private credit investments, and given the effect that credit drying up can have on the economy, expect to see increased scrutiny from regulators. Regulators are likely to conduct reviews. The outcome might be slightly increased ongoing requirements on private credit investors (funds and banks) to take measures that help avoid losses from fraud by their borrowers.